Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThis cash-generative oil producer has huge potential

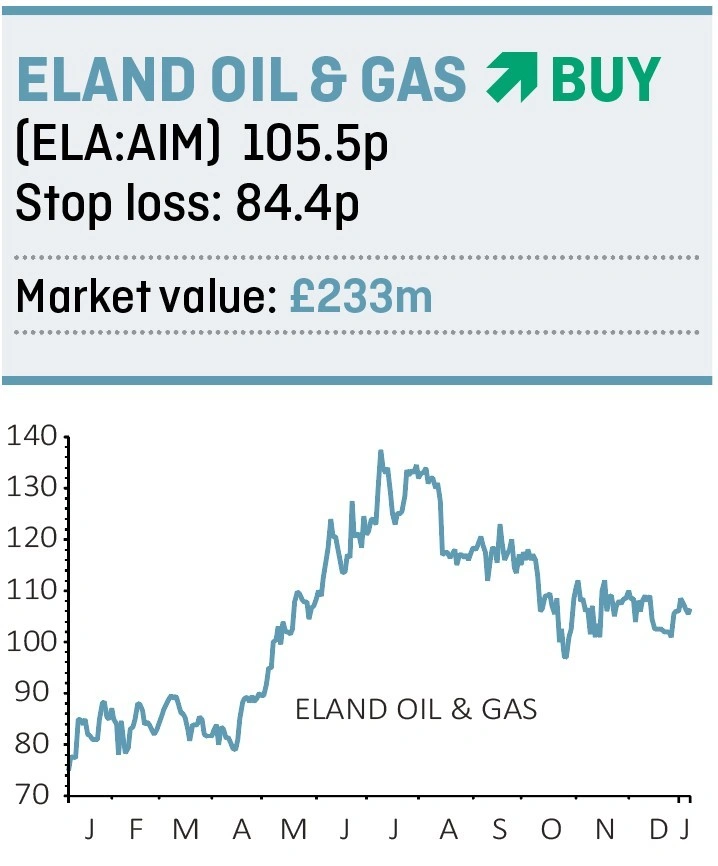

The potential for significant production growth and exploration success at Nigerian oil producer Eland Oil & Gas (ELA:AIM) in 2019 makes this a must-have share for investors with an appetite for high-risk stocks.

We previously flagged Eland as a Great Idea in April 2017 and the shares are now trading at nearly twice the 57p level at which we first highlighted the scope for upside.

The advance in the shares has been matched by operational progress on its OML 40 licence. It has seen robust output expansion with 13,500 barrels of oil per day coming from the Opuama field on

the licence.

As such, we view Eland as much more than a speculative oil play as it is a genuinely cash generative business, and one which house broker Peel Hunt forecasts could be sitting on net cash of $125.3m by the

end of the year.

ANOMALOUS VALUATION

Peel Hunt’s forecasts imply an EV/EBITDA (enterprise value-to-earnings before interest, tax, depreciation and amortisation) ratio of 0.6-times.

While oil price volatility and the possibility of delays leaves forecast earnings open to revision, this still seems like an anomalous valuation and one which could move upwards through the course of the year as Eland delivers on its work programme.

Central to this programme is development drilling on

the Gbetiokun field. This is expected to deliver gross production of 15,000 barrels of oil per day from an early production system and the company says it could ultimately deliver output of 45,000 barrels of oil per day.

Although it boasts a long history of oil production and has well established fiscal terms there are clear challenges, particularly around security in Nigeria.

Investors can take some reassurance from the fact the company has demonstrated its ability to deal with these issues. For example, when the Forcados oil terminal, which currently takes its crude, was shut down due to militant attacks in 2016 and 2017, Eland found an alternative route to market by shipping its oil in small tankers.

It is also worth bearing in mind that a company of Eland’s size would probably not be able to secure an interest in assets of this scale and quality in more stable operating environments.

In the third quarter of 2019 the company plans to drill a well on its Amo-1 prospect targeting up to 78m barrels of oil equivalent, providing a further catalyst for the share price.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.