Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

“Sales per outlet per week are still rising from last autumn’s lows, pricing is still firm and the balance sheet still net cash, but investors are showing no interest shares in Crest Nicholson, despite their lowly valuation,” says AJ Bell investment director Russ Mould.

“They are even shrugging off how the FTSE 250 firm is clawing back £11.1 million from third parties for defective design and workmanship, presumably relating to fire-safety remediation issues, and focusing instead on how investment in IT, new offices for regional expansion and pay increases for staff mean total administrative costs will rise by £10 million to £60 million in the year to October 2023, some £5 million more than expected.

“That is a tidy sum when compared to consensus forecasts for annual operating profit of £73 million (going into the interim results) and may well be raising fears that chief executive Peter Truscott has a bigger-than-expected job on his hands when it comes to turning around the housebuilder’s fortunes.

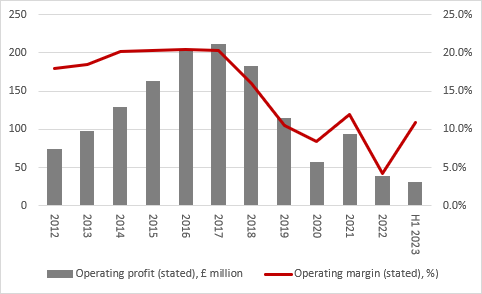

“Crest Nicholson’s earnings and profit margins peaked in 2017 – well before the pandemic and lockdowns, let alone rising interest rates and the end of Help-to-Buy – thanks to operational miscues. The announcement that it will require greater investment than initially thought to open up new avenues for growth and upgrade customer service may deter investors impatient for improved performance, even if the need to pay higher salaries is entirely understandable.

“This could only magnify fears about the wider housing cycle, as inflation refuses to die down as hoped and potentially force interest rates to stay higher for longer than expected, at a time when housing affordability is a key issue, thanks to the combination of lofty prices and higher mortgage rates.

Source: Company accounts. Fiscal year to October

“That difficult combination is reflected in the 18% drop in completions in the first half. Add in higher costs and operating profit and margins are down on an underlying basis, adjusting for last year’s fire cladding remediation costs, which resulted in a loss in the first half a year ago.

“The statement is not all doom and gloom, however.

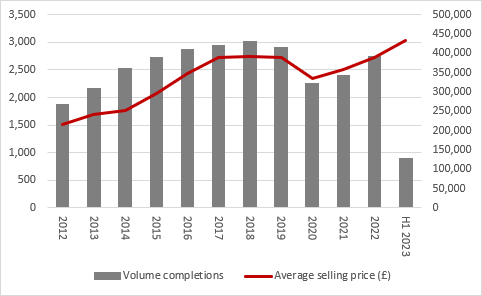

“Perhaps most importantly, Mr Truscott notes further improvements in sales. Crest Nicholson’s April trading statement, for the five months from November to March, noted a sales per outlet per week figure of 0.52 for the second half of that period compared to 0.35 in the first few weeks. For the entire six-month period to April, the sales per outlet per week (SPOW) number was 0.54, although that was still some way down on 2022’s equivalent number of 0.72 and was achieved across ten fewer sites, at 48. Pricing is still firm, too.

Source: Company accounts. Fiscal year to October

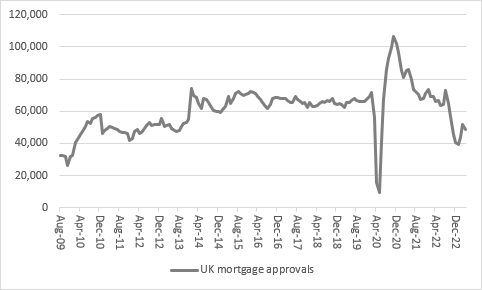

“Sceptics may wonder how long that will last, as UK mortgage approvals weaken again and the average UK house price of £286,532 (according to Halifax) represents 8.5 times the average national salary of £33,384 (according to the Office for National Statistics). Mortgage approvals are back to 2011 levels, before then Chancellor of the Exchequer George Osborne artificially goosed demand (but not supply) with the Help-to-Buy scheme.

Source: Bank of England, Refinitiv data

“It is therefore easy to see why Crest Nicholson share price is wobbling. However, it is also possible to make the case that a lot of bad news is already in the price, especially as the builder is insisting that its net cash balance sheet means it can pay an unchanged dividend of 17p a share in fiscal 2023 – analysts had been factoring in a big cut.

“That sum equates to a chunky dividend yield of 7.6%, which could catch the eye of income-seekers, especially patient ones who look to the cash pile for comfort and believe that demand for quality dwellings will continue to outstrip supply over the long term.

“In addition, Crest Nicholson’s £575 million market capitalisation compares to net assets of £877 million. That 35% discount to book value could go a long way to pricing in even a deep housing downturn.”

| Historic Price/NAV(x) |

2023E PE (x) |

2023E Dividend yield (%) |

2023E Dividend cover (x) |

|

|---|---|---|---|---|

| Crest Nicholson | 0.66 x | 9.8 x | 7.6% | 1.35 x |

| Vistry | 0.71 x | 9.5 x | 6.2% | 1.69 x |

| Bellway | 0.81 x | 6.9 x | 5.9% | 2.44 x |

| Barratt Developments | 0.85 x | 11.5 x | 5.3% | 1.64 x |

| Redrow | 0.87 x | 11.2 x | 3.9% | 2.32 x |

| Taylor Wimpey | 0.92 x | 11.6 x | 7.8% | 1.11 x |

| Persimmon | 1.14 x | 12.3 x | 4.9% | 1.67 x |

| Berkeley Homes | 1.41 x | 11.2 x | 5.8% | 1.54 x |

| Average | 0.97 x | 10.5 x | 5.9% | 1.63 x |

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

These articles are for information purposes only and are not a personal recommendation or advice.

Ways to help you invest your money

Put your money to work with our range of investment accounts. Choose from ISAs, pensions, and more.

Let us give you a hand choosing investments. From managed funds to favourite picks, we’re here to help.

Our investment experts share their knowledge on how to keep your money working hard.

Related content

- Tue, 17/12/2024 - 10:20

- Thu, 07/11/2024 - 11:00

- Wed, 06/11/2024 - 12:06

- Mon, 21/10/2024 - 16:26

- Wed, 09/10/2024 - 10:17